Nest is a defined contribution pension scheme in the UK that manages assets of more than £21.4 billion on behalf of 11.1 million members, who make up a third of the UK workforce.

It was set up by the UK government in 2010 to support its programme for auto-enrolment into pensions in the workplace.

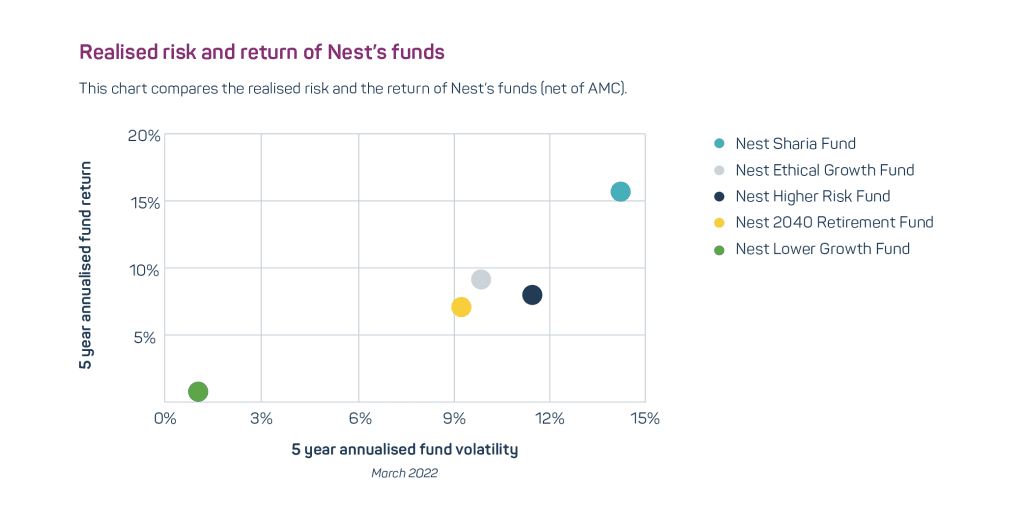

Nest maintains an in-house investment team of 40 professionals, which oversees over 50 default funds and 5 fund options. The vast majority of assets go into the default investment Strategy, which 98 per cent of its members adopt. Outside asset managers provide specialist expertise across both public and private markets. These include Amundi, Blackrock, BNP Paribas, Octopus Renewables, CBRE Caledon and GLIL.

Environmental, social and governance (ESG) considerations have been embedded into the scheme since its inception. Stephen O’Neill, Head of Private Markets at Nest, notes that Nest had “a blank sheet of paper” when it came to determining the best investment approach for a new defined contribution (DC) pension scheme.

- Sustainable investment features of the scheme include:

- Evaluating all mandates on their strength of their ESG/ responsible investment credentials

- Investing in private market assets, such as green infrastructure and social housing.

- An in-house stewardship approach focusing on issues that are most financially material to Nest and its members’ investments, such as climate change and workforce issues

- Exclusion of certain industries including tobacco and controversial weapons

In addition, Nest appointed progressive trustees drawn from a social advocacy background and the European asset management industry (which is well used to meeting the sustainability requirements of Nordics pension schemes). This has helped drive a forward-thinking approach to sustainable investment.

Nest’s commitment to sustainable investing has also been helped by ESG considerations becoming a legally required component of trustees’ fiduciary duty. Equally, its approach has been reinforced by mounting empirical evidence that taking account of ESG factors has a positive impact on an investment portfolio’s risk-return ratio.

Appraising fund managers

Nest considers Asset managers’ approach to ESG risk management and responsible investment when evaluating them across all mandates – private and public.

The breadth and depth of in-house investment expertise – and its strong sustainable investment focus – has now

been built up, partly to reduce the need to call on third-party consultants to help select fund managers or advise on investment strategy.

Nest’s manager selection scoring takes into account quality, price and sustainable investing. All criteria have a pass mark, which is subjectively applied. For example, if a manager comes through financial due diligence but the Nest team doesn’t feel the fund manager’s approach to responsible investment fits with their own, they will score below that threshold and be removed from the process, says O’Neill.

Accessing private markets

Sustainable private markets investments – specifically infrastructure, social housing, private debt and private equity – are core allocations in the scheme’s responsible investment approach.

Nest’s scale and prominence within the DC market, says O’Neill, have allowed it to approach asset managers to create bespoke strategies in these asset classes on highly competitive all-in total expenses’ bases that may not be offered to smaller schemes. This has been key to including these assets into the portfolio while still keeping Nest’s member charge to 0.3 per cent.

Investing in social housing and renewable infrastructure

Investment in UK social housing is primarily in the form of infrastructure debt in a portfolio managed by BlackRock.

In March 2021, Nest appointed Octopus Renewables, part of Octopus Group, to boost its investment in clean energy infrastructure. Octopus Renewables is the largest investor of utility-scale solar power in Europe, as well as a leading UK investor in onshore wind and biomass.

The Nest mandate targets deployment into renewable energy projects and associated infrastructure, predominantly in the UK and Europe. By investing directly in green energy generation, Nest aims both to secure stable, long-term returns for its members and offset carbon- generating investments elsewhere in the portfolio, such

as airport assets. The scheme aims to become a net zero carbon emissions pension scheme by 2050 at the latest.

Rising renewables prices

The rising price of certain renewables requires investment to be highly selective. Offshore windpower, for instance, isn’t included in the Octopus portfolio because of its expense/ risk profile. Conversely, by building as well as buying onshore wind power, Octopus can originate its own dealflow and directly get the benefit of other investors, such as oil majors, bidding up prices.

O’Neill points out that while prices of renewable assets have risen, this has been somewhat mitigated by decreasing operating costs. This has enabled assets to work harder for better margins. Nest estimates it is receiving a net yield on its renewable energy assets of 6-10% compared to 4.5% for public equities, which compellingly demonstrates the value of this asset class to its members’ long-term returns.

Pricing availability

DC schemes’ requirement to provide daily pricing is a challenge when it comes to holding illiquid assets such as energy infrastructure that can only be priced quarterly.

O’Neill says Nest has accepted the risk that 15-20% of its total portfolio may carry a stale price for up to three months. That can be an issue if pricing needs to be calculated mid- quarter (e.g. to calculate benefits for a deceased member) at what transpires to be a premium to fair value. But Nest’s scale, with 11.1 million members, is again a benefit here – the impact of any single instance of cross-subsidy is, as O’Neill puts it, “vanishingly small”.

O’Neil and his team have, however, talked to fund managers about creating intra-quarter pricing for private market assets during severe market events. Given these assets are priced off discounted cashflows, he feels only a serious move in the discount rate would feed through to asset valuations.

Paving the way for other schemes

O’Neill says Nest hopes to be among the first of many defined contribution pension schemes to offer members the diversification and return benefits available through sustainable/responsible investing that are beyond public equity and bond markets. Nest is supportive of government initiatives that will help smooth the way for pension schemes to access the long-term return potential in private markets at the right price for auto-enrolled members.

The issues of cost, liquidity, and the availability of pricing for private markets for DC schemes are real, but, as Nest has shown, they can be overcome. What is required is: extracting competitive pricing from fund managers, using positive cashflows to ensure sufficient liquidity, and having an agreed basis on which to manage stale pricing.

Looking forward, O’Neill says Nest is pushing harder on issues such as climate change. This is something that he believes is becoming easier to do in the UK. He notes that more and more stakeholders recognise a moral obligation not only to help members to build a healthy retirement pot, but also to help deliver a world that’s worth spending one’s retirement in.

Impact investing – and a requirement on trustees to consider a ‘triple bottom line’ on every investment they hold – is still some way off in the world of defined contribution pension schemes. Trustees will need far greater resources before an impact approach becomes widely and effectively adopted.

Nonetheless, by having greater access to private markets and a clear sustainable investment vision and framework, defined contribution pensions can – alongside their defined benefit peers – play a core role in delivering the global green economy.