In the fourth and final part of our series on future-proofing institutional investment, we explore the first steps investors such as pension funds and insurers can take to start incorporating impact into their investment portfolio.

Over the first three parts of this series, we have laid out the case for impact investing. We’ve looked at why a growing volume of institutional assets are flowing into impact investment to improve long-term financial resilience.

We’ve seen how impact strategies enhance long-term return potential by investing in megatrends at the heart of the global economy. We’ve also learnt how companies generating positive impact can (and do) outperform – often contracyclically – as demand for goods and services that can solve urgent problems grows.

The case for impact investing is robust. Assuming key stakeholders, such as trustees and boards, are convinced of its value, what are the first steps to embed impact into a portfolio? Here are six initial actions to consider.

1. Know what you own

A first step is to audit to what extent you already hold impact investments in your portfolio. Investments in renewable energy, companies involved in smart waste management, regenerative agriculture, educational technology or social housing may already be present – but are simply classified as good investments, not impact ones.

When auditing for impact, it’s vital to understand the difference between companies ‘not doing harm’ versus those actively doing good. There are a lot of resources to explain how impact goes beyond both responsible and sustainable investment – and all stakeholders need to know the distinction.

A useful guide is the ABCs of Impact. Originally developed by The Impact Management Project (now Impact Frontiers), this categorises investments that: A – Avoid harm to stakeholders; B – Benefit stakeholders; C – Contribute solutions to solving some of the world’s greatest problems. Ideally all investments in an institutional portfolio will fall comfortably into any one of these three categories. Over time, an impact approach will see more and more capital allocated to tranche C.

2. Agree what impact you want to have

The next consideration is what type of impact you want to have. For many large institutional investors seeking to spread risk, the answer may be to have a highly diverse set of target impacts addressing a wide range of social and environmental challenges. For others, there may be logic in aligning with the institution’s own activities. For example, insurers with exposure to weather-related risks may want to focus on investments to decarbonise the global economy. Zurich Insurance Group, for instance, has built an impact investment portfolio of $11 billion across green, social and sustainability bonds and infrastructure investments supporting climate and community resilience1.

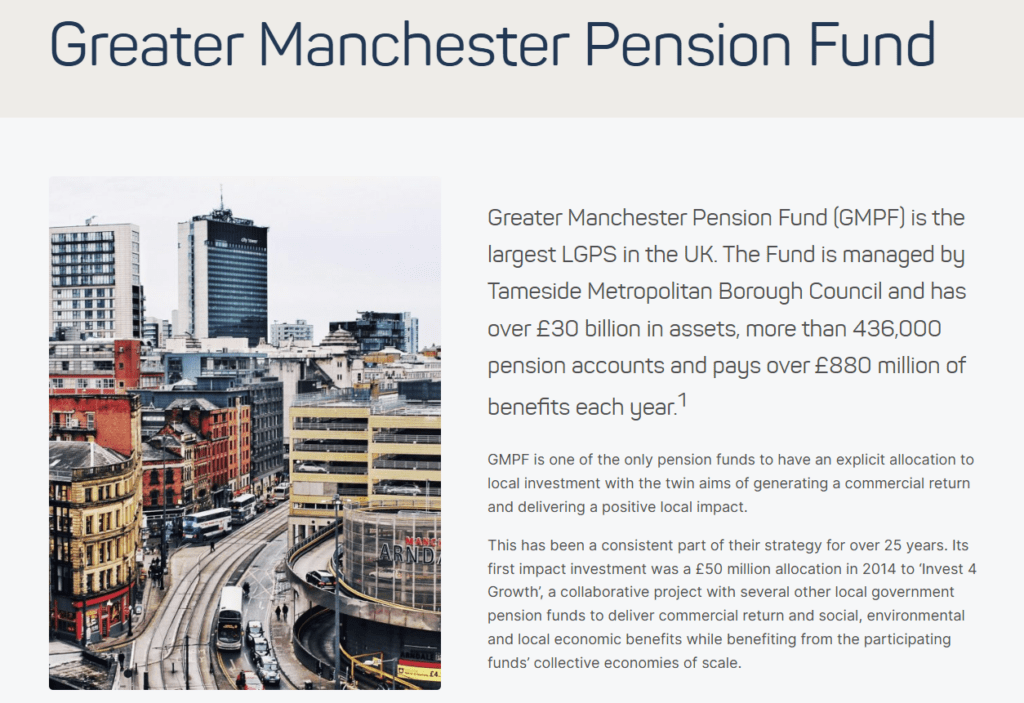

For pension funds, the focus may be closer to home. Local authority pension schemes may want (and are being strongly encouraged) to invest in housing, skills and employment initiatives that directly benefit their local communities. The Greater Manchester Pension Fund has been a pioneer in this type of place-based investing. Through its Impact Portfolio and property venture fund (GMPVF), it has deployed more than £1 billion into housing, infrastructure and SME finance while targeting returns of RPI +4%2.

The UN Sustainable Development Goals (SDGs) offer a widely-used framework for identifying which impacts to prioritise and for communicating intention and progress to stakeholders. There’s a growing array of case studies that show how pension funds, endowments and other investors have mapped their impact intentions to the SDGs.

Of course, this work to align mission to impact can go far deeper. You may wish to develop a ‘theory of change’ around the activities, outputs, outcomes and impacts your institution wishes to deliver through its investment capital. Such work can provide internal and external clarity to your goals and help to translate your broad impact goals into an actionable investment strategy.

3. Consider how much to allocate to impact

Impact investing never needs to be an ‘all or nothing’ decision. Many institutional investors start with a small allocation – say 5%-10% – either as an allocation within an existing portfolio or as a carve-out with a new specialist impact manager. Often the priority will be to transition out of those investments that are furthest from delivering positive impact (such as those with material negative impacts).

The key is to make sure the impact allocation isn’t so small that it is sidelined or has too few investments to demonstrate its potential. Instead, you want to be able to see how these initial approaches might eventually direct the broader portfolio. A transition to impact is often done in stages, depending on the liquidity of the investments being acquired/divested from. A gradual but steady increase in allocation to impact can also be sensible to allow all stakeholders to get comfortable with this new approach and build up a record of quarterly return.

4. Consult on appropriate investments

The next step is to see how impact goals can translate into investable opportunities. For defined benefit pension funds and many insurers, the choice of appropriate impact investments will depend heavily on which assets can be relied on to meet very specific liabilities.

As we have pointed out previously in this series, the good news is the wide and growing range of asset classes and investment vehicles that can be used to target impact – from venture capital and private equity, to sovereign green bonds and private credit, and, in the real asset space, property and infrastructure projects. Meanwhile ‘blended finance’ solutions can provide scope to align opportunity to specific risk parameters.

5. Draw up an investment policy statement

Many of the points above will, of course, need to be codified into an Investment Policy Statement (IPS). An IPS is essential to translate ambition into guidelines for investment managers and ensure the strategy is adhered to, whatever the market conditions.

The key difference between an impact-enabled IPS compared to a traditional IPS is that –alongside return expectations, liquidity requirements, risk tolerance, and target asset allocation – the document will provide equal detail on impact intent and how this is to be enacted, measured and reported on. The process of creating an IPS can therefore be invaluable in ensuring all stakeholders are clear and aligned on why and how the organisation is investing for impact.

6. Consider what additional expertise is needed

As the steps above show, introducing impact investment to an institutional portfolio involves embracing new thinking about long-term goals, choice of investments and measuring and reporting on results achieved.

Many institutions will come to the conclusion that they need external expertise to help them embark on their impact journey. The ‘lightest touch’ outsourcing involves introducing impact-focused funds/managers to an existing portfolio. But some groups may want far deeper support to help revise their investment policy and strategy. This may require a whole new Request For Proposal (RFP) process to shortlist and select new advisers or investment service providers. The key here is to be as rigorous as possible, challenging potential providers on their impact expertise as much as their financial capabilities.

This process is a major investment of time and resources. But it’s worth remembering that every RFP is also an opportunity to influence the broader financial services sector. By highlighting and setting expectations for impact investing expertise, your RFP process can ultimately help to push up standards across the industry.

Other considerations

These are just a few steps involved in introducing an impact approach to a portfolio. Other considerations will include: education and communication both internally and externally; measuring and reporting on impact; and how to evolve the investment policy as new impact opportunities open up.

There is a lot to think about. But as many investors attest, the key to investing in impact is just to get started. However modest or ambitious your organisation’s impact goals are initially, a wealth of tools, resources, support and peer networks exist to assist you on your journey, including via the Impact Investing Institute.

The opportunities to drive positive real-world change while delivering on financial mandates have never been greater. With no end in sight for geopolitical upheaval, embracing impact could be key to delivering the long-term resilience that every institutional portfolio needs.

Sources:

1. Zurich Insurance Group. (n.d.).

Impact investment.

Retrived 4 March 2025

2. The Good Economy. (2025).

GREATER MANCHESTER PENSION FUND

ANNUAL ASSESSMENT OF THE PLACE-BASED

IMPACT OF GMPF’S LOCAL INVESTMENT PORTFOLIO.